The forex carry trade strategy is one of the most enduring and institutionally studied approaches in currency markets. Unlike momentum or technical breakout strategies, carry trading earns you money while you hold a position — not just when you exit it. The core idea is elegant: borrow a currency from a country with low interest rates, convert it into a currency from a country with high interest rates, and pocket the difference every day through swap or rollover credits. Over time, that daily income compounds into meaningful returns. But elegant does not mean safe. Carry trades can unwind violently when risk sentiment shifts, and exchange-rate losses can erase months of accumulated interest in a single session. This guide covers the mechanics of the forex carry trade, how to calculate your daily swap income, which pairs to watch, the risks that have historically wiped out leveraged carry traders, and a disciplined step-by-step approach for trading it properly.

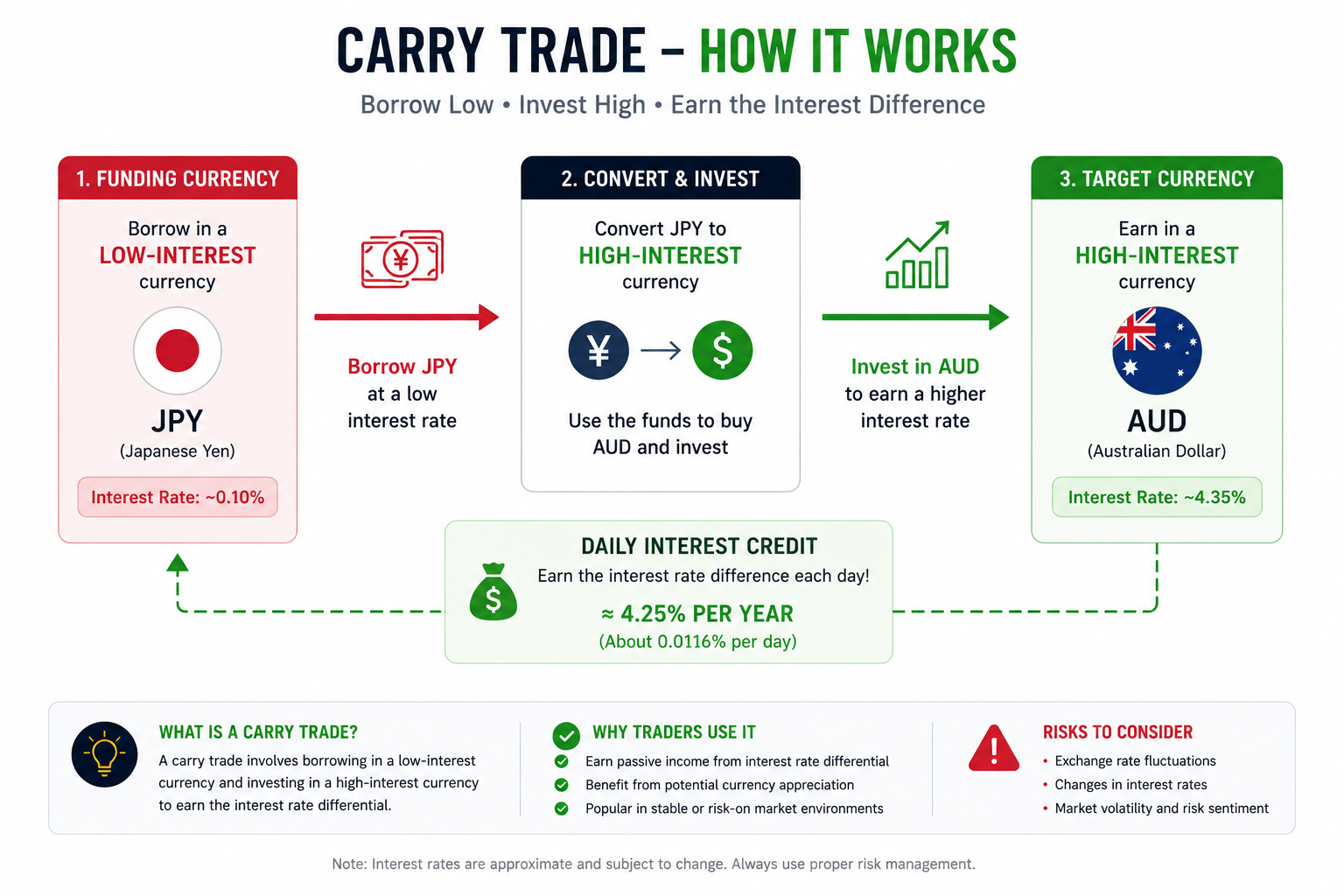

Fig 1.1Forex carry trade strategy diagram

What Is a Carry Trade and Why Do Traders Use It

At its most basic level, a carry trade finances a position in a higher-yielding asset by borrowing in a lower-yielding one. In foreign exchange, it takes the form of a simultaneous position across two currencies with meaningfully different interest rates set by their central banks. When you hold a currency position overnight, your broker credits or debits a swap that reflects the difference between the interest rate of the currency you are long and the one you are short. If you are long a currency with a 5% policy rate and short one with a 0.1% rate, you earn roughly the 4.9-percentage-point difference, prorated daily. That daily credit is the heartbeat of the forex carry trade strategy.

Every carry trade has two legs. The funding currency is the one you borrow — it carries a low interest rate. The target currency is the one you buy — it carries a higher rate. Historically, the Japanese yen has been the world’s dominant funding currency, while the Australian dollar, New Zealand dollar, and emerging market currencies like the Mexican peso have been preferred targets because they offer higher rates, reasonable stability, and sufficient liquidity.

How Swap Rates Are Calculated

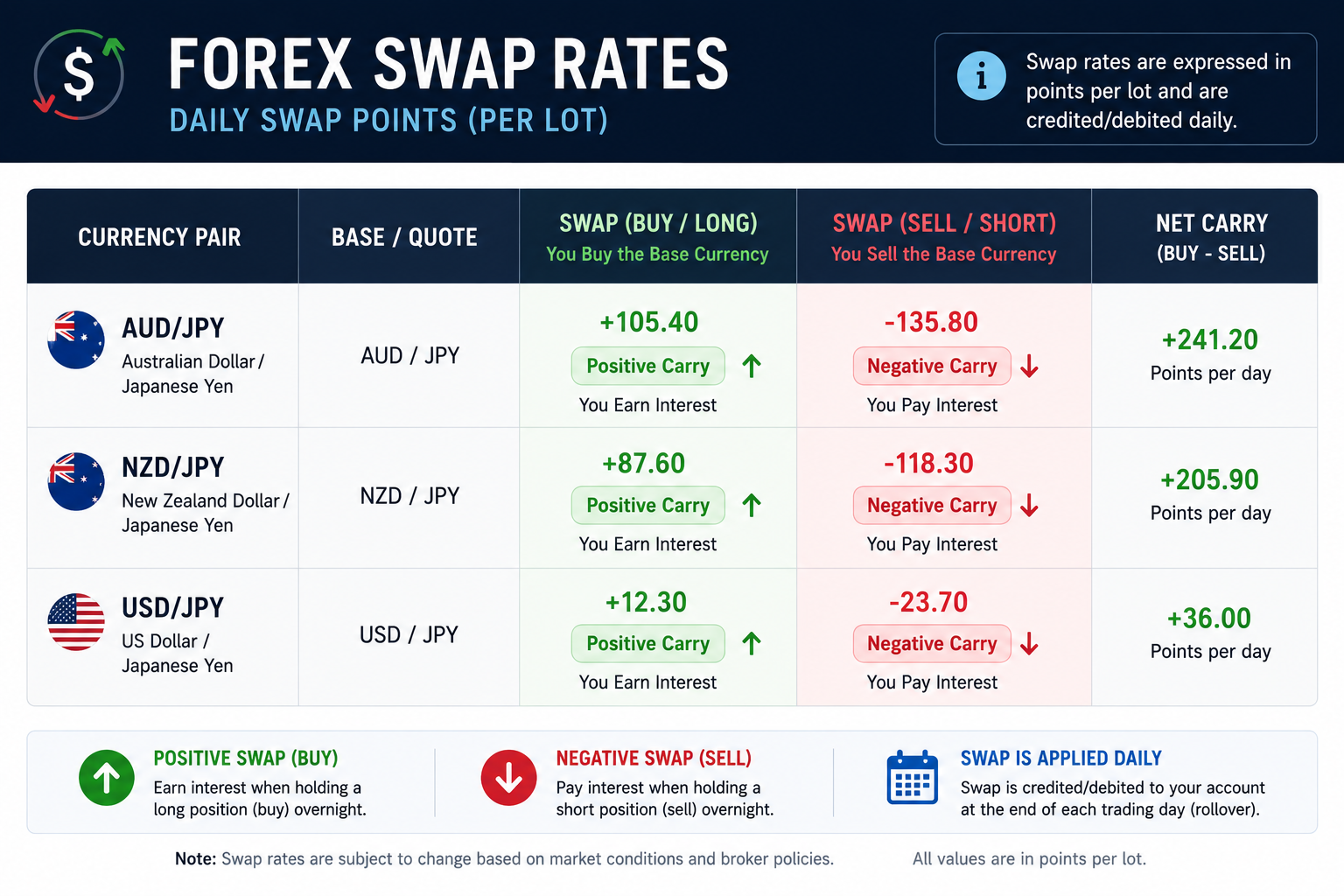

The daily swap rate your broker credits or charges is not simply the central bank rate divided by 365. It incorporates the broker’s own spread on the overnight lending rate, the tom/next rate from the interbank market, and in some cases a markup, so the effective rollover is slightly lower than the raw differential suggests. The swap is typically applied at 5:00 PM New York time, and on Wednesdays it is tripled to account for the weekend settlement period. For a positive carry position you earn the differential; for a negative carry position you pay it.

Fig 1.2 Swap rate table for forex carry trade pairs

Classic Carry Trade Currency Pairs

A viable carry pair needs three things: a meaningful interest rate differential, sufficient liquidity, and a long-term exchange rate that is not in structural free-fall. The G10 carry pairs — AUD/JPY, NZD/JPY, and to a lesser extent GBP/JPY — are the most widely traded. Emerging market carry pairs offer higher differentials but come with substantially more volatility and political risk.

| Currency | Typical Role | Rate Environment | Carry Direction |

|---|---|---|---|

| JPY (Japanese Yen) | Funding | Very low (0–0.5%) | Short (sell) to fund |

| CHF (Swiss Franc) | Funding | Low (0–1%) | Short (sell) to fund |

| AUD (Australian Dollar) | Target | Moderate-High (3–5%) | Long (buy) for carry |

| NZD (New Zealand Dollar) | Target | Moderate-High (3–5.5%) | Long (buy) for carry |

| MXN (Mexican Peso) | Target (EM) | High (8–11%) | Long (buy) — higher risk |

The entire carry framework rests on central bank policy. When the Bank of Japan signals continued accommodation while the Federal Reserve or Reserve Bank of Australia tightens, the differential widens and carry trades become more attractive. A surprise rate hike by the Bank of Japan can cause a sudden and painful carry unwind as traders rush to cover short yen positions simultaneously.

The Real Risk: Carry Trade Unwinds

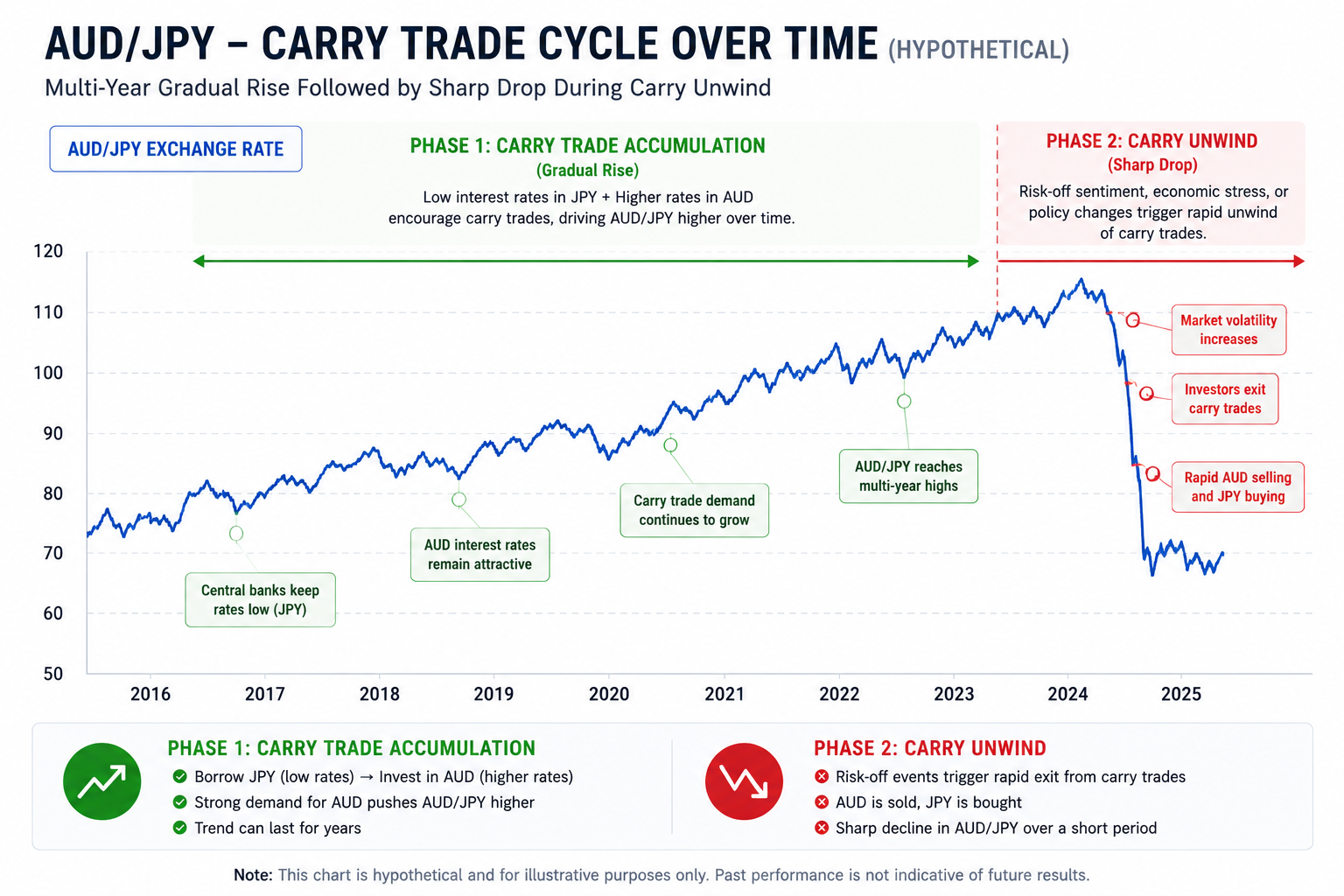

A carry unwind happens when risk sentiment deteriorates sharply — a financial crisis, a geopolitical shock, or a sudden surge in the VIX. Leveraged investors around the world simultaneously close their carry positions, buying back their funding currency and selling their target currencies. Because so many participants hold similar positions, the unwinding is self-reinforcing: exchange rates can move 5–10% in hours, wiping out months of accumulated rollover income in a single day.

The most dramatic carry unwind in modern memory occurred during the 2008 global financial crisis, when the yen surged over 30% against the Australian dollar in roughly three months. A more recent example occurred in August 2024, when an unexpected Bank of Japan rate hike triggered a sharp yen rally and a global risk-off event as the JPY carry trade unwound rapidly. Researchers Markus Brunnermeier, Stefan Nagel, and Lasse Pedersen documented this dynamic in their 2008 paper “Carry Trades and Currency Crashes.”

Standard theory predicts high-interest currencies should depreciate by exactly the interest differential, leaving zero profit — this is uncovered interest rate parity. In practice, it consistently fails: high-yielding currencies tend to hold steady or appreciate during calm periods, an anomaly economists call the forward premium puzzle. The failure of this parity is the fundamental reason the forex carry trade can be profitable, but the distribution is sharp: long periods of slow gains punctuated by sudden, severe crashes.

Fig 1.3 AUD/JPY carry trade unwind chart

Step-by-Step Approach to Trading the Forex Carry Trade

First, identify the rate differential: a gap of at least 2–3 percentage points is generally the minimum worth targeting, and you should check your broker’s published swap table rather than the headline policy rate. Second, confirm the trend is in your favor using higher-timeframe technical analysis — the strategy works best when the target currency is appreciating or holding steady against the funding currency. Third, assess global risk sentiment via the VIX: when it is low and falling, carry trades tend to perform well; above 20–25, unwind risk rises.

Fourth, size the position for survival. Leverage is the carry trader’s greatest enemy; many professionals operate at 3:1 or less and size positions so a 10–15% adverse move does not threaten the account. Fifth, set a stop loss on the weekly chart rather than the 15-minute chart, since short-term noise will stop you out of a position that is fundamentally sound. Sixth, monitor central bank calendars and reduce or hedge exposure before major Bank of Japan meetings.

Common Mistakes in Carry Trading

Chasing yield without checking liquidity is a frequent error — emerging market pairs like TRY/JPY offer massive differentials but can move 15–20% against traders in days due to political crises or intervention. Ignoring the cost of the spread relative to the swap is another: on some exotic pairs the bid-ask spread extends the effective breakeven weeks or months into the future. Finally, many traders confuse positive carry with a safe trade — a trade can have positive carry and still be deeply losing if the exchange rate moves against you. The swap income is supplemental to a well-reasoned directional view, not a replacement for one.

What Top Traders and Research Say

Kathy Lien’s Day Trading and Swing Trading the Currency Market dedicates substantial coverage to the forex carry trade, explaining how professional traders combine carry analysis with macroeconomic positioning and technical confirmation, and emphasizing that entering late in a risk-on cycle when positions are already crowded dramatically increases unwind risk. The academic grounding comes most rigorously from Brunnermeier, Nagel, and Pedersen’s 2008 paper “Carry Trades and Currency Crashes,” which shows that carry returns are positively skewed in calm markets but subject to crash risk driven by the simultaneous unwinding of crowded positions.

On the practitioner side, veteran trader and analyst Ashraf Laïdi has noted: “Carry trades live and die by risk appetite.” That compression of the strategy’s essence is difficult to improve upon.

Frequently Asked Questions

What is carry trade in forex?

A carry trade in forex is a strategy where a trader borrows a currency with a low interest rate — the funding currency — and uses the proceeds to buy a currency with a higher interest rate, the target currency. The trader earns the difference between the two rates, called the interest rate differential, paid out daily through the swap or rollover credit. A trader long AUD/JPY is effectively borrowing yen at a near-zero rate and investing in Australian dollars at a higher rate, with profit accumulating as the position is held open.

What are the best currency pairs for a forex carry trade strategy?

The most liquid and widely used carry pairs are AUD/JPY and NZD/JPY, where the Australian and New Zealand dollars serve as target currencies and the yen as the funding currency. USD/MXN (held short to receive the peso’s higher yield) is a popular emerging market carry pair. The best pair depends on the current rate environment, the broker’s actual swap rates, your risk tolerance, and the prevailing trend on higher timeframes.

How much can you earn from a forex carry trade?

The raw income depends on the size of the interest rate differential, the position size, and how long you hold it. On a standard 100,000-unit AUD/JPY position with a 4% differential, the daily rollover credit is roughly $110 before the broker’s markup. But this is meaningless without accounting for exchange-rate risk — a 5% adverse move can wipe out more than a full year of carry income, which is why position sizing matters more than yield maximization.

Why do carry trades crash so suddenly?

Carry trades attract many participants simultaneously because the strategy is systematic and well-known. When risk sentiment turns negative, all of these traders attempt to exit at the same time, and the funding currency surges as everyone rushes to buy it back. This self-reinforcing dynamic, formally described as carry trade crash risk, produces sharp, asymmetric moves where stops are skipped, liquidity evaporates, and losses compound in hours.

Is the forex carry trade strategy suitable for beginners?

The forex carry trade strategy is generally not recommended as a first strategy. While the concept is simple, the risk management required to survive carry unwinds demands experience and a solid understanding of macroeconomic forces. It is better approached after a trader has experience with position sizing, reading risk sentiment, and using central bank calendars. Starting with a small, lightly leveraged position in a liquid G10 carry pair with a defined weekly-chart stop is a more responsible entry point.

How does the Bank of Japan affect carry trades?

The Bank of Japan is the single most important institution for global JPY carry trades because Japan has maintained the world’s lowest policy rates for decades, making the yen the preferred funding currency. When the BoJ signals any shift toward tightening, yen shorts unwind, the yen appreciates, and yen-funded carry trades suffer exchange-rate losses. The August 2024 episode is a vivid recent example, and carry traders must treat every BoJ meeting as a potential risk event.

Final Thoughts

The forex carry trade strategy has survived decades of academic scrutiny and market cycles for a simple reason: the interest rate differential is real, the daily income it generates is real, and the failure of uncovered interest rate parity to eliminate that income is one of the most robust anomalies in financial economics. Used with discipline — realistic leverage, trend confirmation, active monitoring of risk sentiment, and a genuine plan for the inevitable unwind — carry trading can be a meaningful component of a sophisticated forex approach. But it demands intellectual honesty about its risks. This is not a passive income strategy; it requires daily attention to central bank calendars, VIX levels, and global risk flows. The edge is real, the risk is real, and respecting both is what separates traders who profit from carry over time from those who give it all back in a single chaotic week. For more on how professional traders manage carry positions alongside technical and macroeconomic analysis, visit forexmarkettrendss.com.